The future of global retirement

03 Dec 25

The future of global retirement

1 Introduction

About Smart

Smart is a world-leading retirement technology provider. Our mission is to transform retirement, savings and financial wellbeing, across all generations, around the world.

Launched in 2015, our technology platform – Keystone – serves the needs of retirement savers globally, and we are now active on four continents. Keystone is specifically designed to help governments and financial services organisations to serve their citizens' and customers' retirement saving and spending needs.

Smart’s team of engineers, researchers and user experience experts built Keystone based on research from data covering more than a million savers across the globe. Our Future of Global Retirement report summarises a regular piece of research we carry out, gathering insights from thousands of savers on their perceptions toward retirement saving.

We believe in the power of technology to bring positive change.

Smart is one of the fastest-growing financial technology companies in the world. We’re really proud of being able to make a genuine difference.

From day one, we’ve always believed in the potential of starting with a blank sheet of paper and not having to build things to fit ‘legacy’ technology.

2 Foreword

Andrew Evans and Will Wynne

As perceptions of retirement shift across the world, in line with emerging technology and reforms to legislation, the industry needs to keep up and remain one step ahead. At Smart, we’re continuing to lead the way in research and development in this space, and as part of our mission, we’ll continue to share some of the insights we gain around the needs of savers across the world.

In 2021, we launched our first ‘Future of Global Retirement’ report, taking you through findings from more than 6,000 savers across the UK, Australia and the US, discussing their knowledge, attitudes and concerns about retirement saving. This year we look at how some of these trends are progressing, with the inclusion of South Africa, a region on the cusp of pension reform with the aim of decreasing poverty amongst its ageing population.

In 2022 we celebrated the important milestone of reaching a million savers who are now benefiting from Smart’s technology in our Smart Pension Master Trust. And at the beginning of 2023, Smart has exceeded £5 billion in Assets Under Management (AUM) on its proprietary Keystone platform. These are incredible achievements and represent our commitment to transform retirement savings for the better.

As we enter 2023, we bring you our latest Future of Global Retirement report. Understanding people’s behaviours and attitudes to saving for later life, helps us to make sure that our platform is constantly evolving to keep savers and technology at the forefront of everything that we do.

As before, we want to share this information with a view to serving our mission: to transform retirement, savings and financial wellbeing, across all generations, around the world.

This year’s report includes findings from more than 8,000 savers across the UK, Australia, South Africa and the US. Although the retirement landscape in each of these regions differs vastly, we have identified some common trends. Men and women have different perceptions of decumulation (the process of converting pension savings to retirement income), there are shared concerns around being able to afford basic living costs in retirement and an increasing desire for transparency, flexibility and online access to retirement savings. We hope that shedding light on these concerns and preferences will continue to shape the retirement landscape for the better through technological solutions that have savers’ wellbeing at their core.

Thank you.

3 Methodology overview

Fieldwork, in the form of online surveys, was undertaken in late 2022 in the United States, Australia, South Africa and the United Kingdom. Respondents to these surveys were aged 18+ with no other determining criteria. The research sought to understand current perceptions of retirement in the regions specified with relation to spending habits, preferences in retirement funding and general understanding of retirement options.

Roughly 2,000 respondents per region, over 8,000 respondents in total.

Legislation across the world is continually evolving and changing, with many countries moving towards a defined contribution savings model, where participants are responsible for funding their own retirement. This may have a significant influence on decisions people make about their pension and retirement investments, and their subsequent perceptions of pensions and saving in later life.

Please note percentages in the following tables and charts may not total 100 due to rounding and/or multiple answers selected.

See detailed breakdown of methodologies in Section 11.

4 Retirement perceptions in the UK

It is now a decade since the introduction of auto enrolment in the UK, which has seen millions of people saving for retirement for the first time and opt-out rates below 10%. However, despite the initiative’s success millions are still undersaving, due in many cases to working part-time or being in low-paid jobs. Addressing this may become more difficult now that a cost of living crisis has taken hold in the UK.

Our survey was conducted at a time of particular economic turmoil in the country, as the pound crashed and political leadership changed swiftly. Inflation and rising costs are impacting people’s day-to-day spending and wider budgeting, and it is possible that this will shift focus away from long-term saving towards short-term survival.

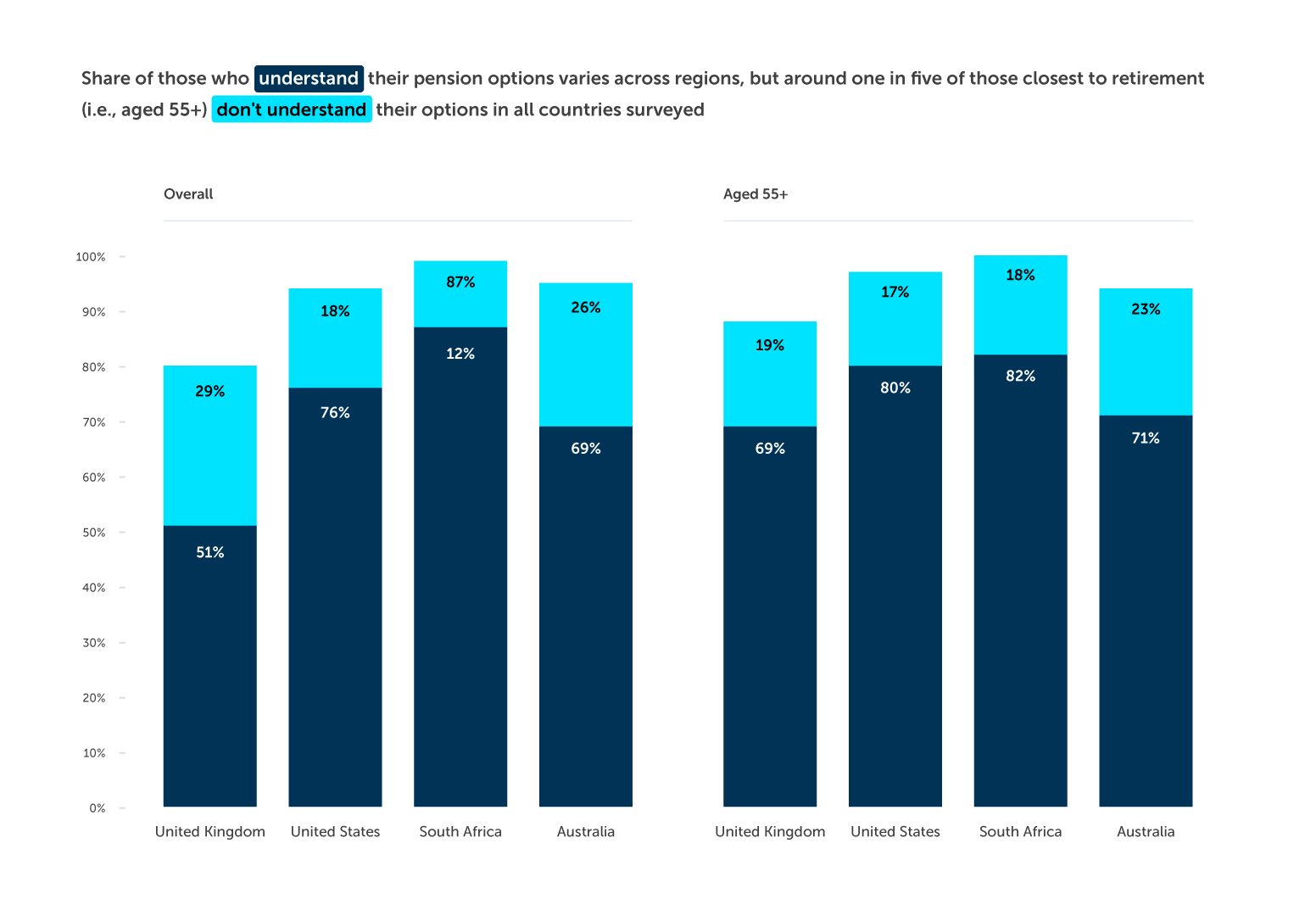

The knowledge gap remains among those nearest retirement

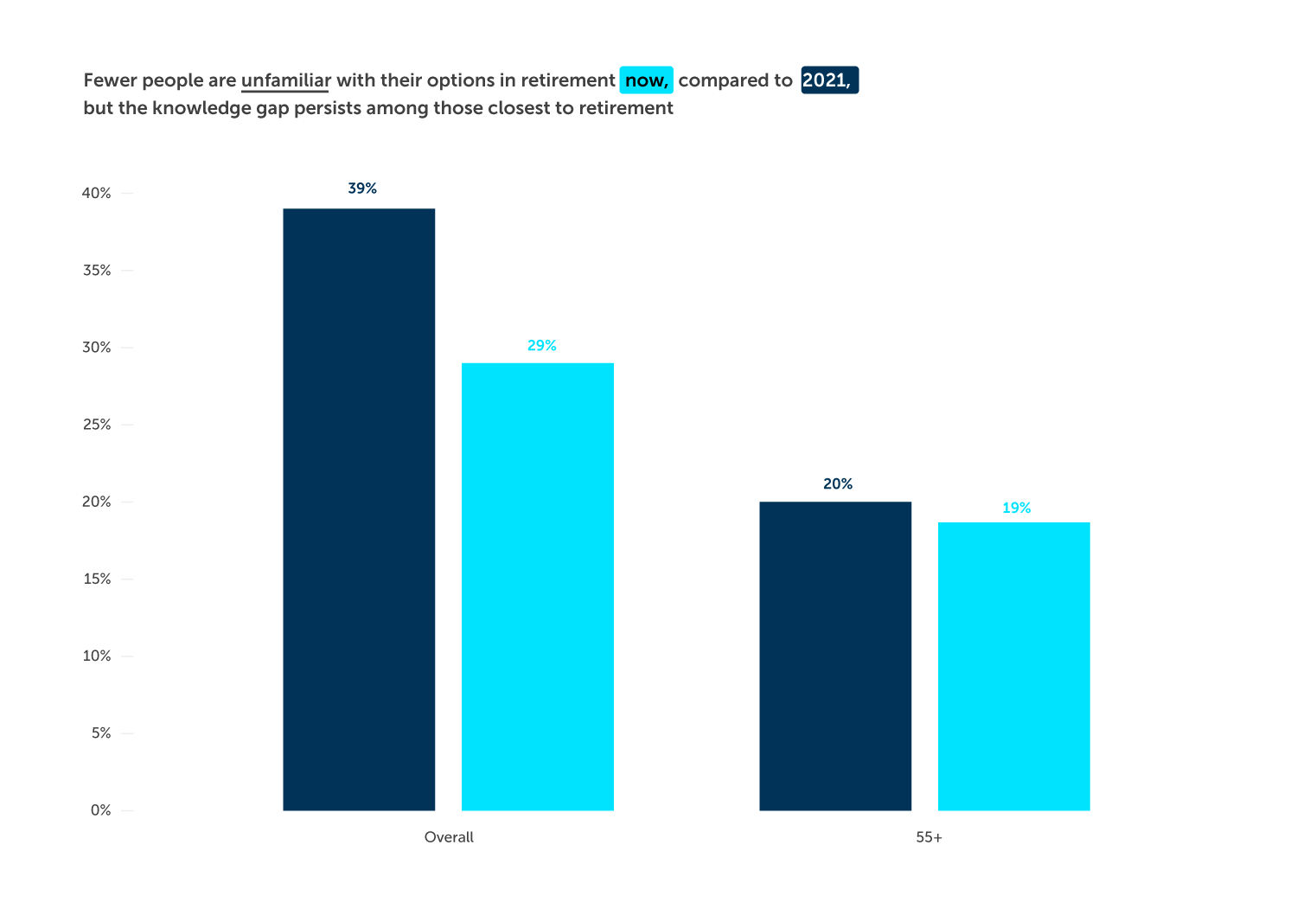

There remains a significant gap in UK respondents’ knowledge of pension planning but it is showing signs of shrinking

Almost one in three (29%) don’t have a clear understanding of the options available to them in retirement. This is down from 39% in our previous survey, but still a significant proportion of UK respondents. The drop in the number who feel they lack a clear understanding is driven by younger respondents, suggesting the possible success of industry efforts to educate younger people as well as the continued positive impact of auto enrolment.

Amongst those closer to retirement age, understanding remains consistent with 2021’s figures. One in five (19%) of those aged 55+ still do not have a clear understanding of their retirement options.

When UK respondents seek advice, their go-to sources are a financial adviser, a government website and pension fund providers. In practice, though, these are not all considered the most useful – friends and family are among their top three most useful sources of information about retirement finances, while pension fund providers are not.

‘Retirement’ is now seen as a fluid concept

People in the UK see retirement as a gradual process

Gone is the idea of reaching a certain age and suddenly stopping work. Around half (47%) of UK respondents see retirement as a transition, rather than a one-off event. This view is more prevalent among women – more than half (51%) see retirement as a transition compared to 43% of men. Unsurprisingly, it becomes more common the closer people get to retirement, jumping from 37% of 18-24 year olds to 58% of 65+ year olds.

Living costs are becoming a harsh reality

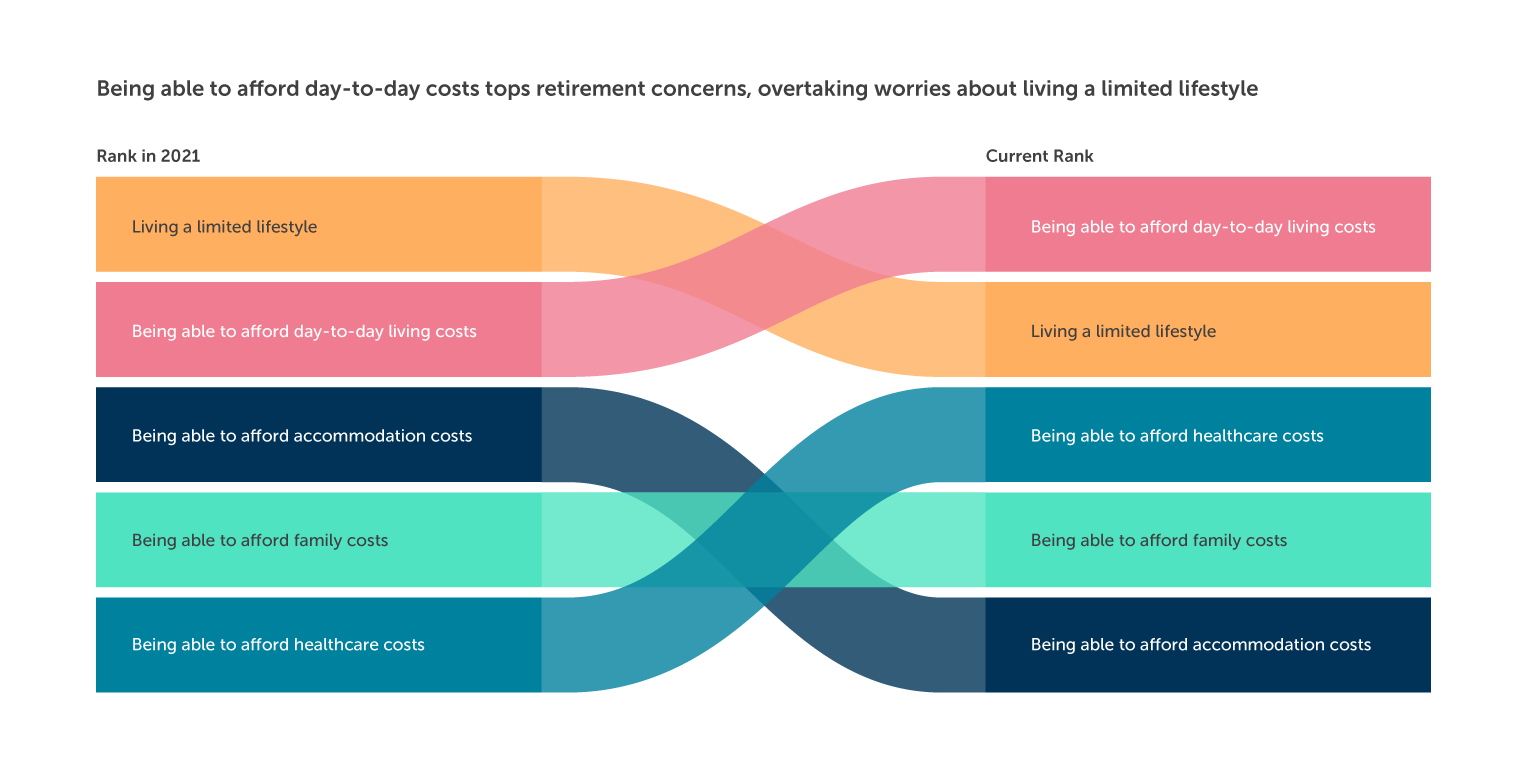

As the cost of living crisis bites, concerns about meeting day-to-day costs in retirement have risen

In 2021, UK respondents’ biggest concern was about having to limit their lifestyle in retirement. This year, their biggest worry is about meeting basic everyday costs.

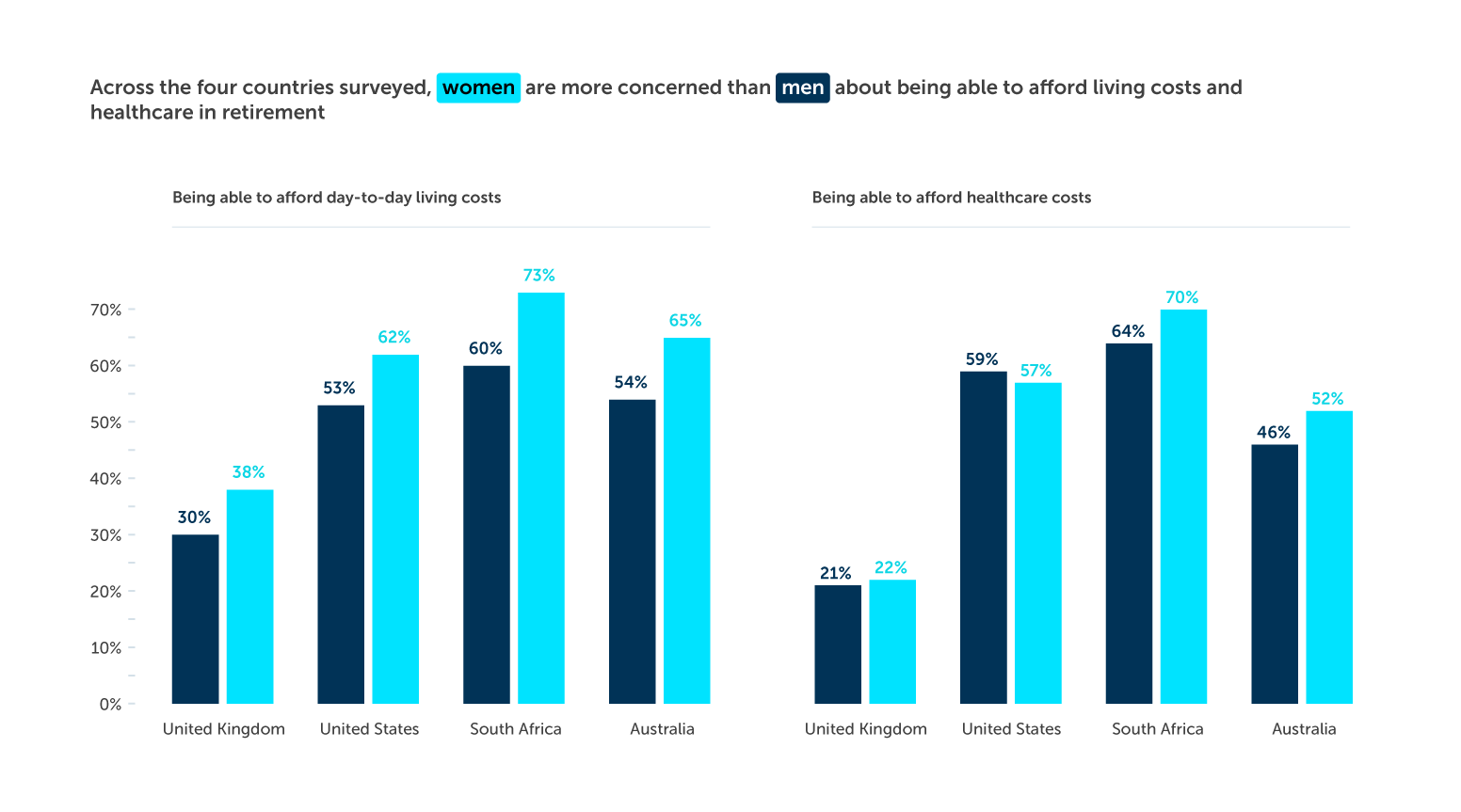

These concerns are heightened for young people and for women. One in five young people (18-25) are concerned about being able to afford accommodation in retirement, compared to just one in ten of their 65+ year old counterparts. And 38% of women are concerned about having enough money for day-to-day living expenses in retirement, compared to 31% of men.

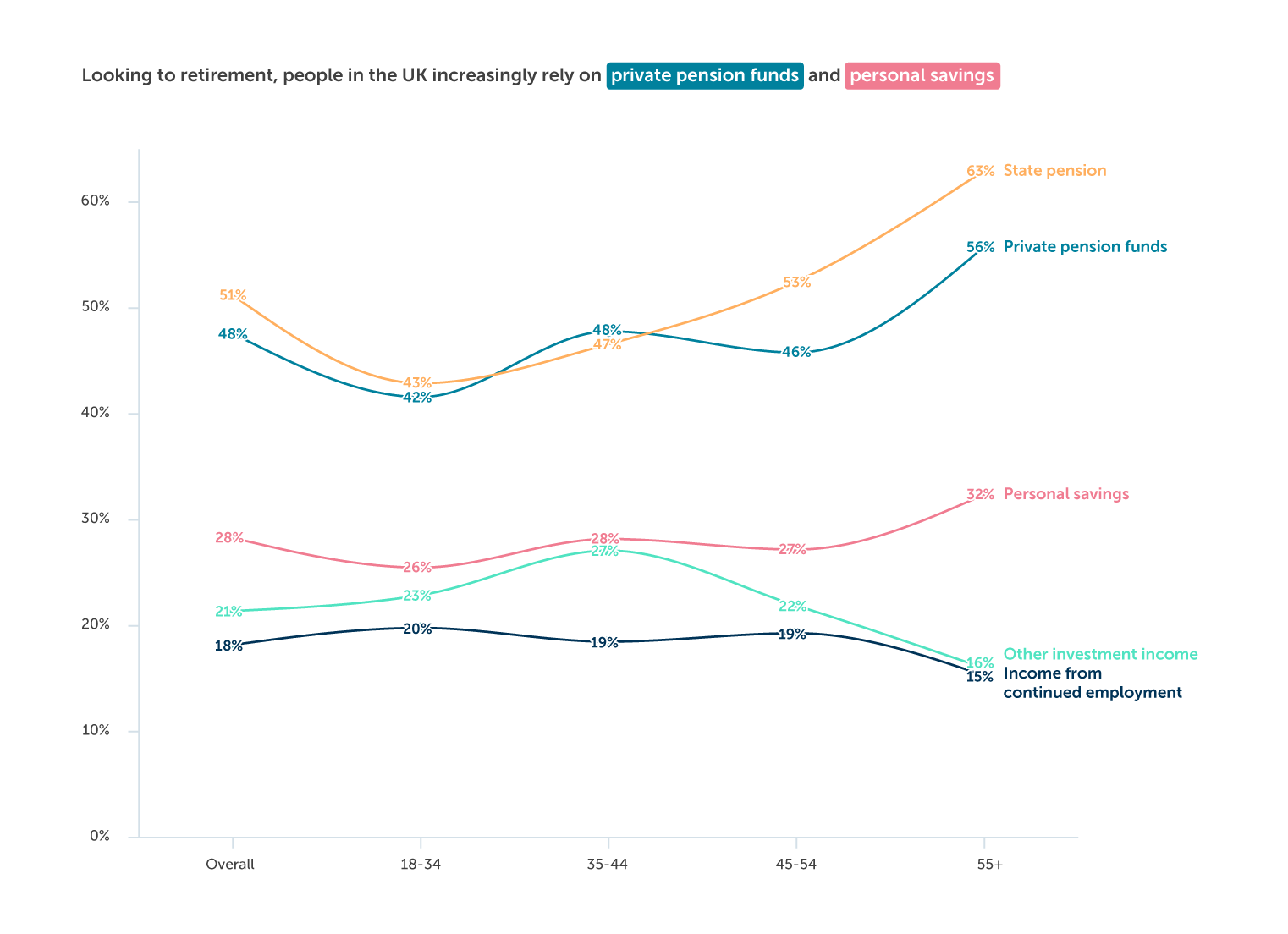

While many expect their living costs to decrease in retirement – perhaps due to slower lifestyles, or anticipating having paid off their mortgage – more than a quarter (28%) expect their expenses to increase. More than half (57%) plan to supplement their pension with other forms of income – for example, through personal savings (28%) or continued employment (18%).

This is particularly true for younger generations. Just 43% of 18-34 year olds expect their retirement to be at least partly funded through a state pension, compared to 63% of those aged 55+. And 42% of 18-34 year olds expect their retirement to be funded by a private pension, compared to 56% of 55+ year olds. This is concerning, given the UK’s ageing population and the fact the state pension is considered too little to live on.

People want control and simplicity

Pension offerings need to provide autonomy while also being straightforward

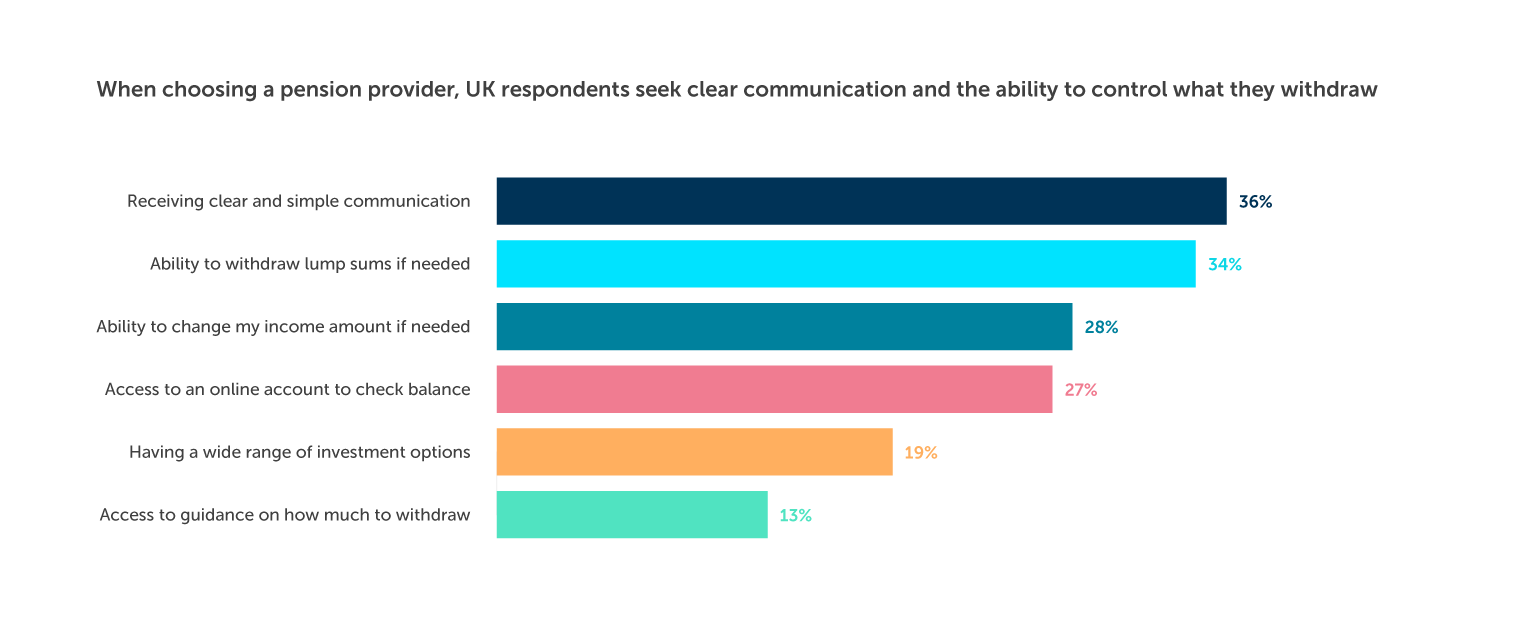

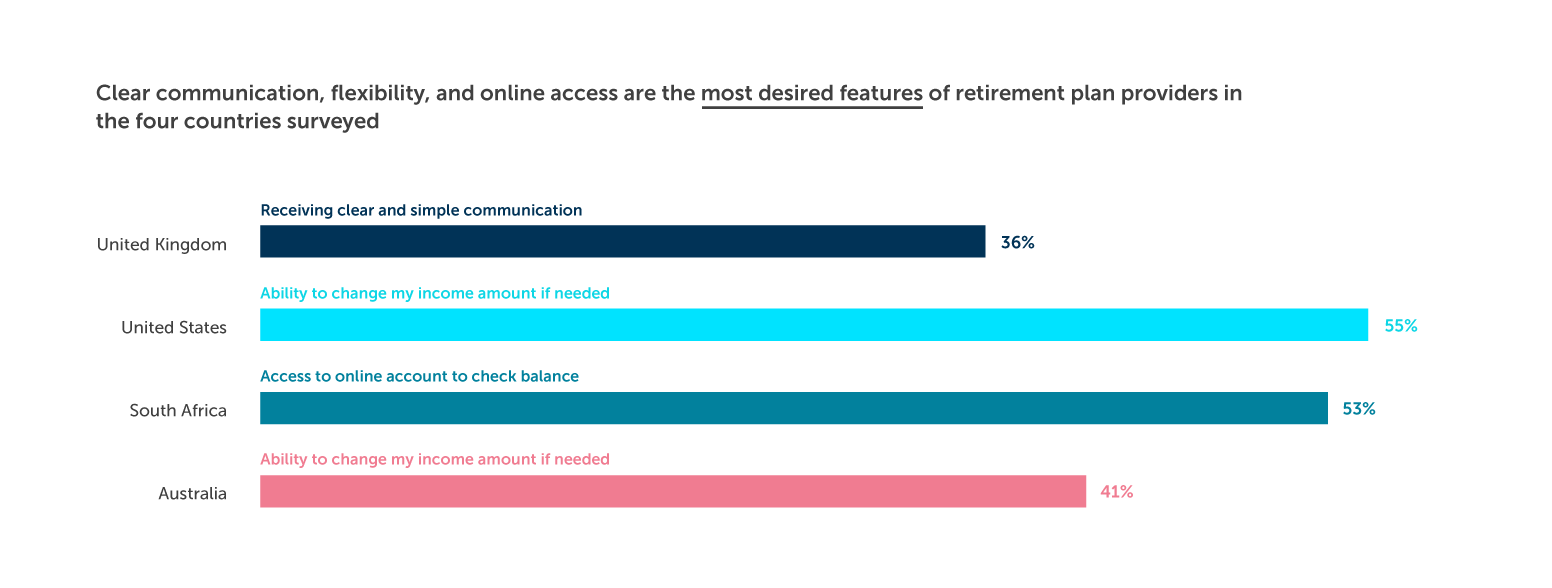

The most important thing that UK respondents want from their pension provider is clear and simple communication, with 36% considering this important. Their desire for pensions to be straightforward and easy to understand is unsurprising, given the knowledge gap we have already seen.

Control is also important to UK respondents – their other priorities when looking for a pension provider include the opportunity to withdraw lump sums as needed (34%), and the option of changing income amounts (28%).

Online access and savings management

In response to the question ‘How important is it to you, if at all, that you will be able to manage your retirement finances online?’, 60% consider it fairly or very important to be able to do so. This figure increases to 72% when excluding those who answered ‘Don’t know’.

Despite – or, perhaps, because of – UK respondents’ limited understanding of their retirement finance options compared with savers in other regions, they are the most keen to manage their own retirement savings entirely single-handedly. More than a third (38%) favour this approach, rather than having some assistance in managing their finances. Just 8% would leave it entirely to someone else.

5 Retirement perceptions in the US

While the US continues to rely for the most part on voluntary provision of retirement plans, new federal and state legislation aims to expand access and reduce the coverage gap.

At the federal level, new legislation called the SECURE 2.0 Act of 2022 was signed into law on December 29, 2022 (after our survey responses were collected), as a part of the Consolidated Appropriations Act. Secure 2.0 expands tax incentives for small employers to adopt retirement plans, includes provisions mandating automatic enrollment and automatic escalation for new plans beginning in 2025 and creates a new type of plan called a Starter 401(k) plan available beginning 2024. It also introduces the "saver's match", a tax credit that will be paid into the retirement plans of participants on low incomes. Together, the package of more than 92 provisions represents a strong step toward making retirement plans available to more American workers.

Some states, such as California, Illinois and Oregon, have introduced their own mandates for employers to offer a plan, and these continue to expand. California, for example, expanded its mandate to cover even the smallest employers from July 2022.

We expect retirement plan coverage to continue to increase gradually, but in the absence of a national mandate it will still remain lower than in many other countries.

Healthcare and living costs remain the top concerns

The need to meet basic costs is a big – and growing – concern

This year’s financial environment has been challenging for retirement savers globally, with rising interest rates, high inflation and falling stock prices. This is likely to have exacerbated savers’ concerns about their ability to meet their retirement spending needs.

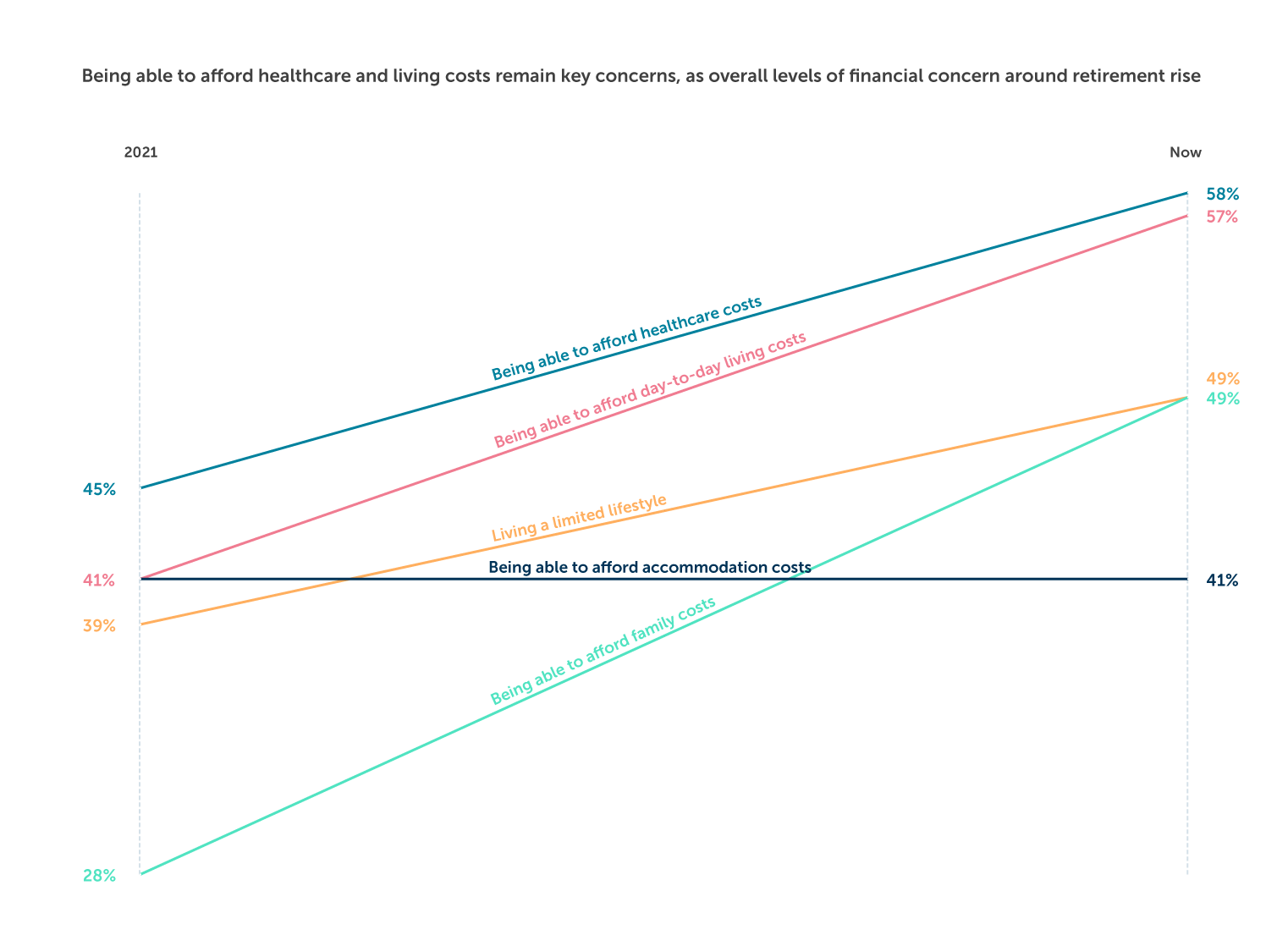

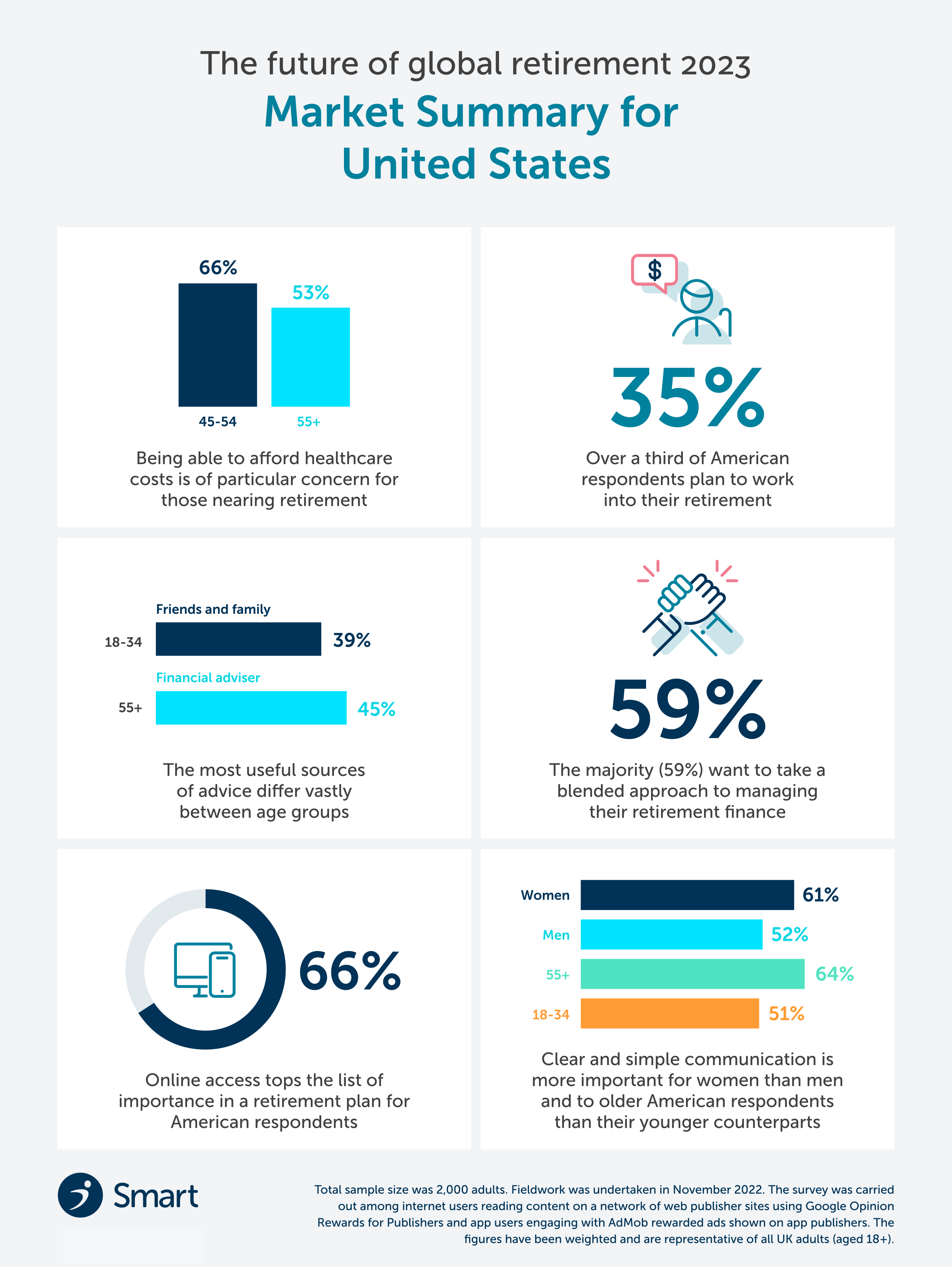

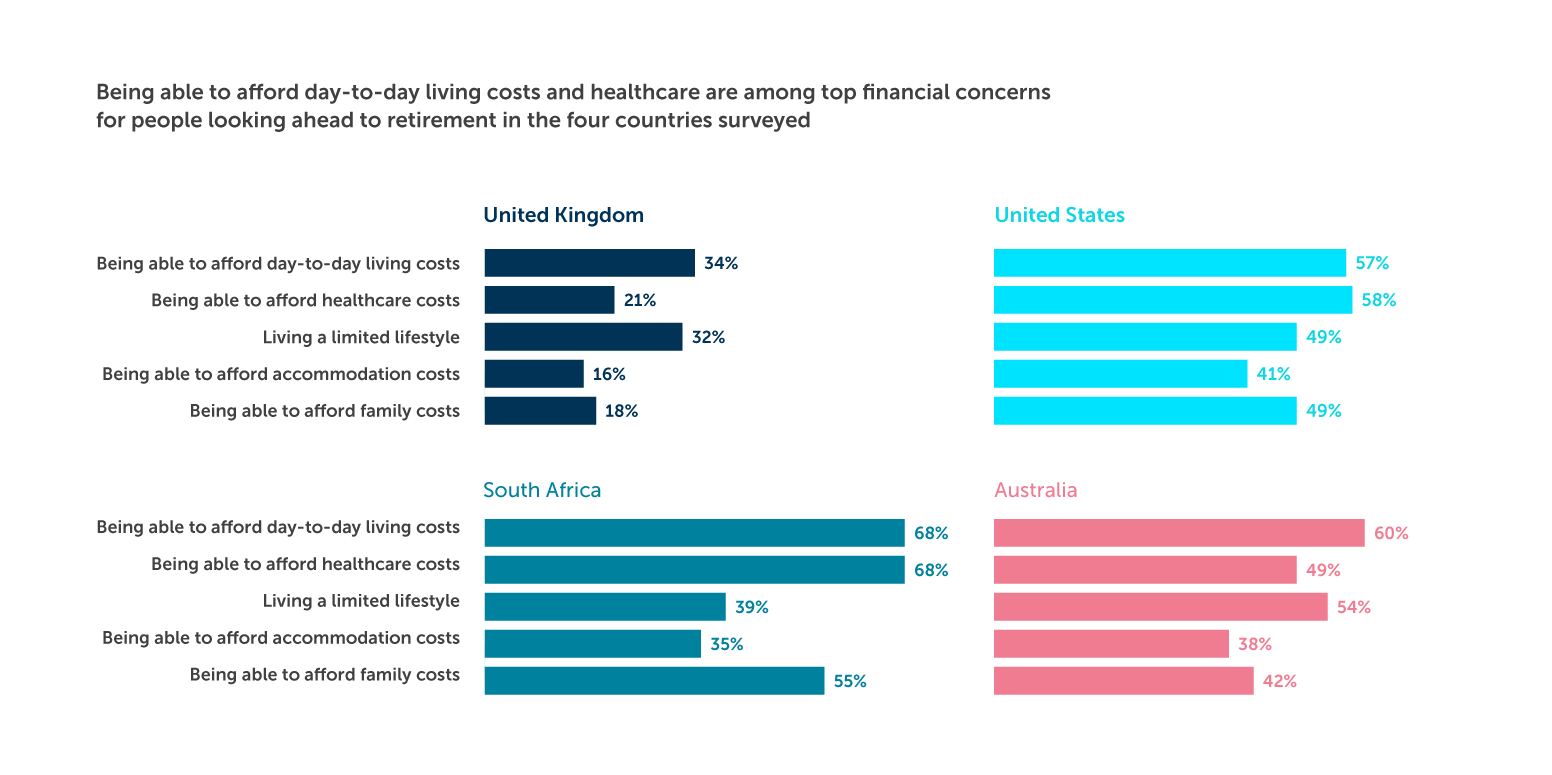

Consistent with our 2021 findings, healthcare remains top of the list when it comes to retirement-related concerns, and worry is growing (58%, up from 45% in 2021). This concern jumps to 66% among those closer to retirement, aged 45-54. Being able to afford day-to-day living costs continues to be the next most common concern (57%), jumping 16 percentage points since 2021.

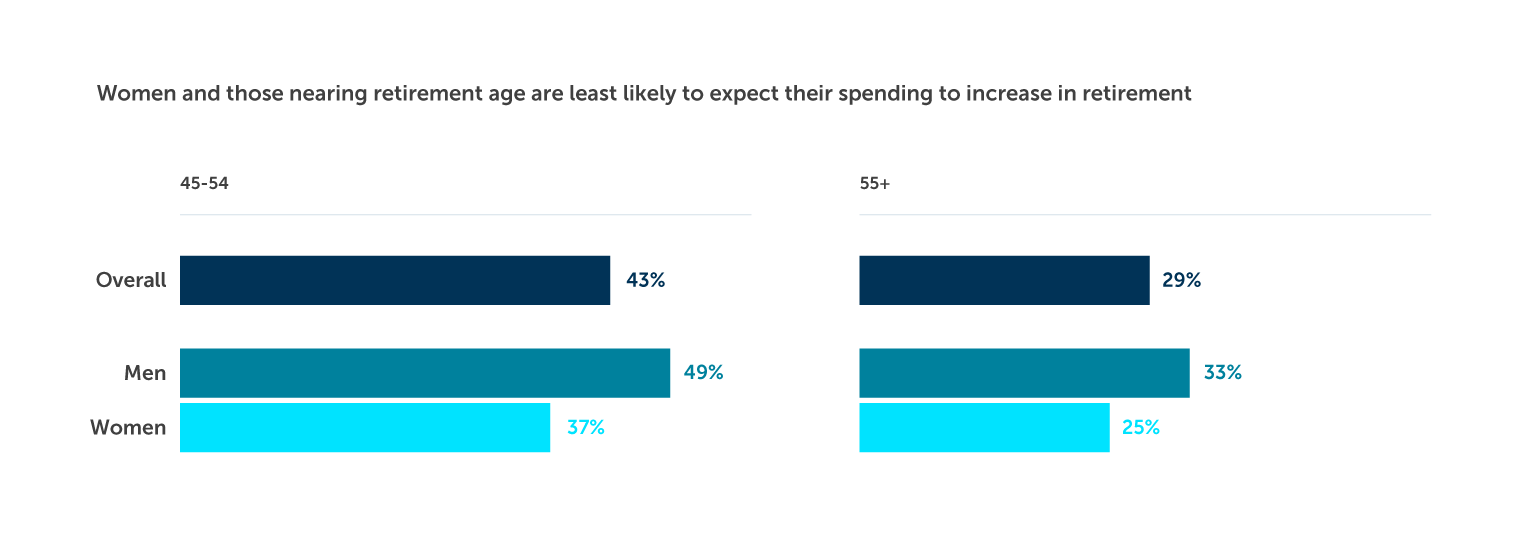

Two in five (43%) people between the ages of 45-54 see their average monthly spend going up in retirement, which could reflect widespread concern about the impact of inflation on day-to-day spending. Men (49%) are more likely to expect their expenses to increase than women (37%). Interestingly, those who are closer to retirement (55+) are less likely to expect their spending to increase. This may be because they have a better understanding of what their spending in retirement is likely to look like.

Around one in five Americans plan to work into their retirement, with 18% saying that income from continued employment will help fund their retirement. This indicates that retirement is increasingly becoming a transition rather than a one-off event. Compared to other age groups, those aged 45-54 are most likely to say they will rely on social security (63% compared to 60% average) and personal savings (64% compared to 58% average), and least likely to say they will rely on income from continued employment (27% compared to 35% average).

Most Americans understand their retirement options

However, sources of advice do not always meet expectations

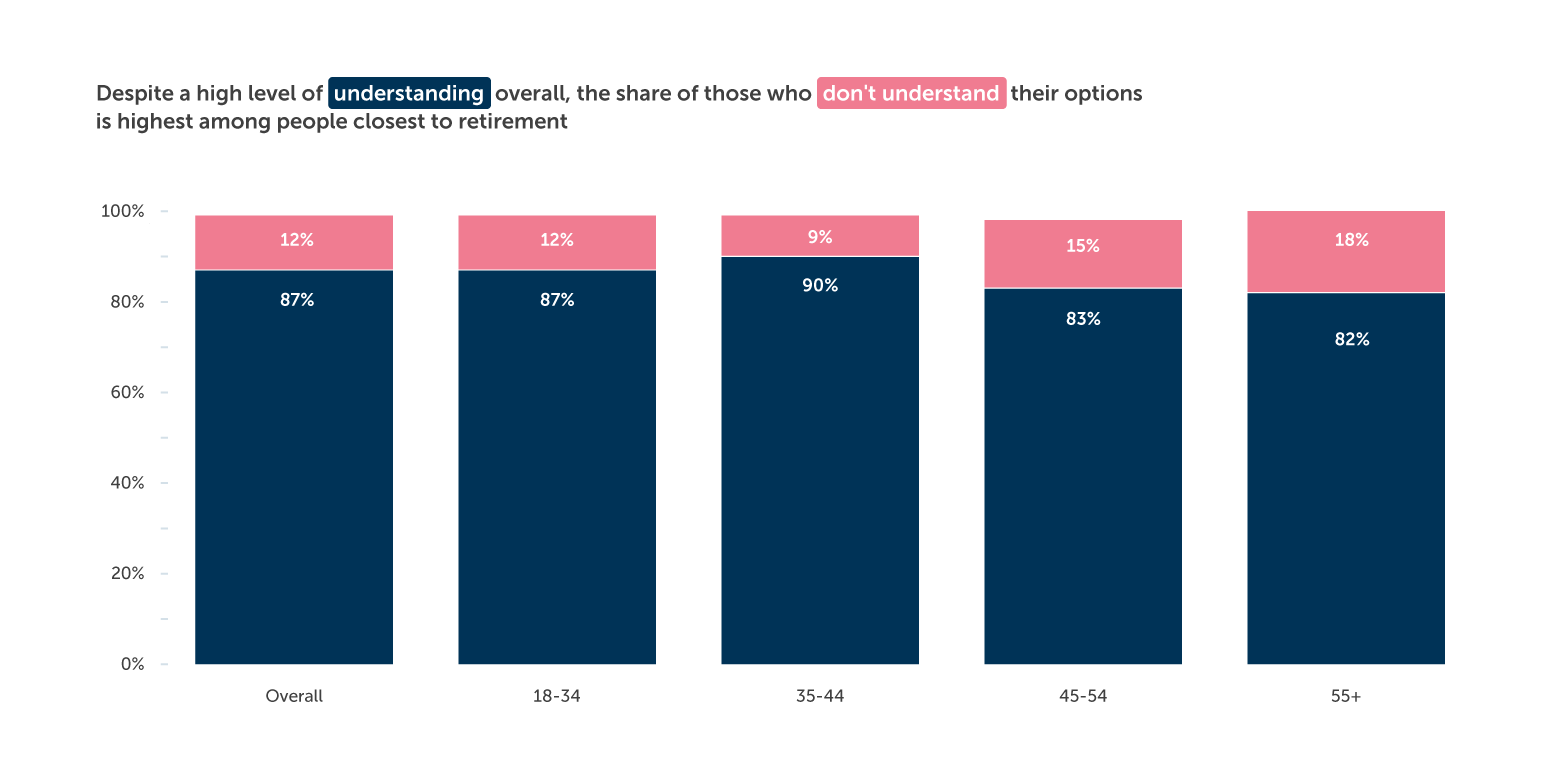

Almost four in five (79%) say that they understand their options for financing their retirement. This is up from just 54% in 2021, suggesting that the knowledge gap may be shrinking.

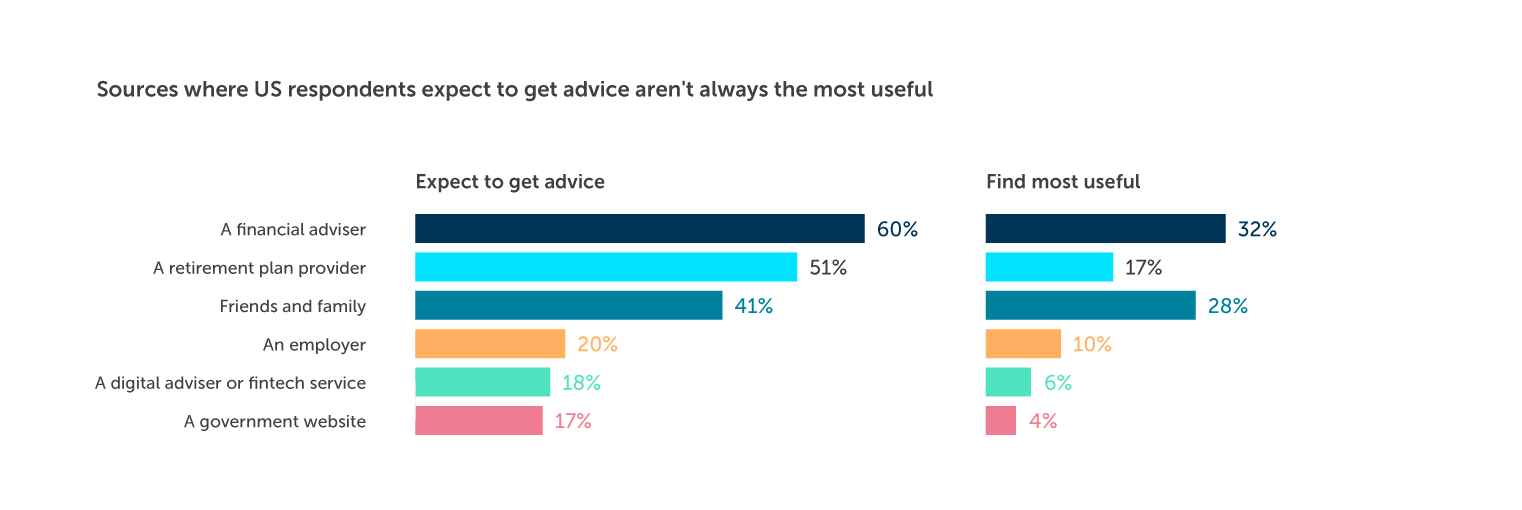

Financial advisers are considered the most useful source of information (32%). They are closely followed by friends and family, with 28% of respondents citing these as the most useful source of information. Unsurprisingly, older participants approaching retirement are most likely to rely on financial advisers, whereas friends and family are the most important source of advice for younger participants.

While 51% of Americans say that they expect to get advice from their retirement plan provider, just 17% say that they receive their most useful advice from their retirement plan provider. Similarly, only 10% mention their employer as their most useful source of advice. This presents an opportunity for service providers to step in with guidance and education.

People want control and support

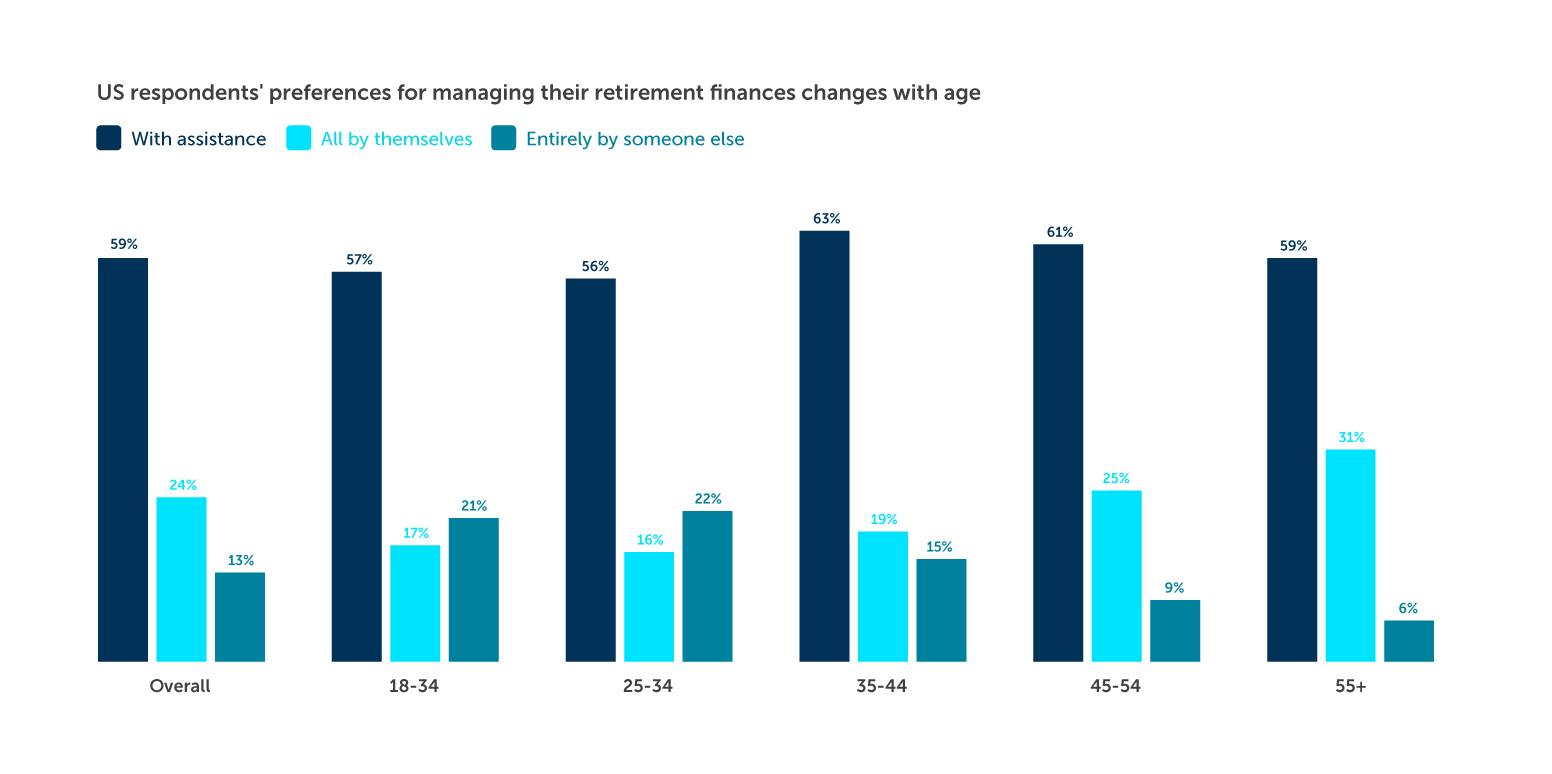

Americans are looking for a combination of autonomy and assistance

When it comes to managing their retirement finances, American respondents are looking for a balance of control and support. Only 6% of those aged 55+ want to put the management of their retirement finances solely in the hands of a third party. The majority (59%) want to take a blended approach – they want to manage their own money in retirement, but they also want assistance when doing so. Fewer people (24%) want to manage their finances completely by themselves. This reflects the complexity of retirement planning, given that most Americans feel they have a good understanding of their retirement options. Even with this understanding, they recognise that managing everything on their own can be hard work and complicated.

The desire for complete control is driven by those aged 55 or older: 31% want to manage their retirement finances entirely on their own, compared to just 17% of younger Americans.

When American respondents consider the most important features of a retirement plan, online access comes at the top of the list (66% select it as important). This reflects their desire for autonomy, as well as the legacy of lockdown measures shifting more and more of life online.

Clear and simple communication comes second (57%), and is more important for women (61%) than men (52%) and to older Americans (64%) than their younger counterparts (51%).

6 Retirement perceptions in South Africa

In South Africa, the second pillar – in which recipients and employers pay into a privately-funded system that allows for lump sum withdrawals – has become well-established and achieved substantial coverage despite being a voluntary system. The government is now considering introducing auto enrolment, although these details remain at an early stage.

The current system is undergoing a reform that will see the introduction of a ‘two-pot’ model. This will allow South Africans to access cash for emergencies and other short-term needs, while keeping the majority of their savings for retirement. The current system allows regular cashing out when savers change jobs, which is reflected in our findings showing a relatively high number of people withdrawing cash before retirement. The policy goal for the new ‘two-pot’ system is to introduce a shift that will result in more funds preserved for retirement.

There is a clear service gap in retirement finance advice

Financial advisers are the main source of information, with other sources falling short of expectations

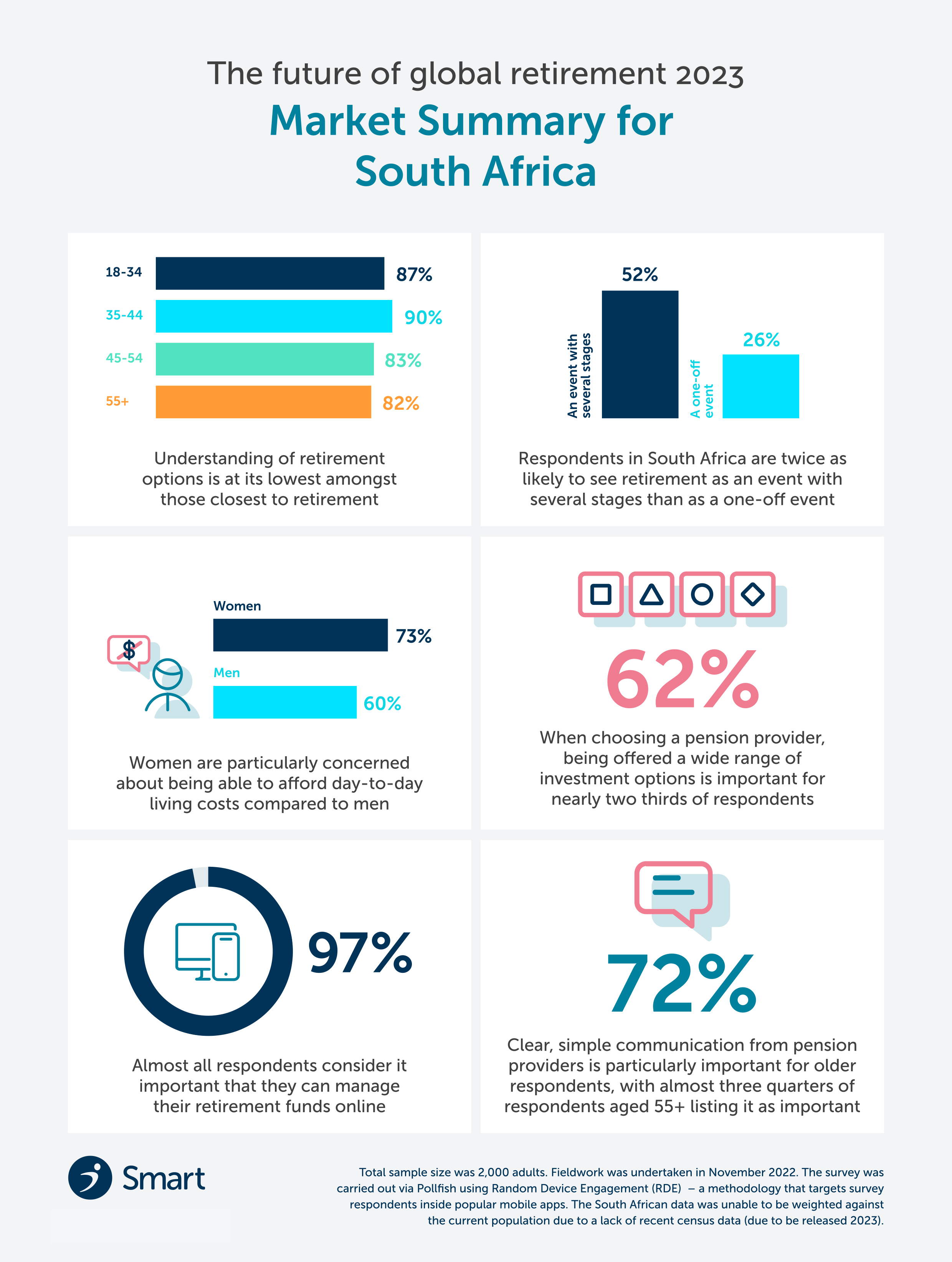

Understanding of retirement finance options in South Africa is generally very strong, with almost nine out of ten (87%) South African respondents feeling they have a good understanding of their options. This is to be expected, given that the current legislation in South Africa is fairly clear-cut. In most instances, it dictates that if you have a pension you can take a certain amount as a lump sum when you retire and the rest as monthly payments. That said, 18% of those closest to retirement (55+) report not understanding their options. It may be that on nearing retirement, people become more aware of the gaps in their knowledge.

A financial adviser is the clear go-to source of retirement finance advice, with 79% of respondents expecting to turn to one. Pension fund providers are a distant second, with just 44% of respondents expecting to turn to them for advice. Older South African respondents are slightly more likely than their younger counterparts to look to a pension fund provider (56% of those aged 55+ compared to 41% of those aged 18-34), or to a fintech service (28% compared to 17%).

Financial advisers are also considered the most useful source of information in practice, with 50% saying they have received useful guidance from one. Pension fund providers sit in third place, at 15%. On the whole, when it comes to providing retirement finance information, pension fund providers, online digital advisers and employers are not currently meeting South Africans’ needs.

‘Retirement’ is a fluid concept

Most think of retirement as a gradual process

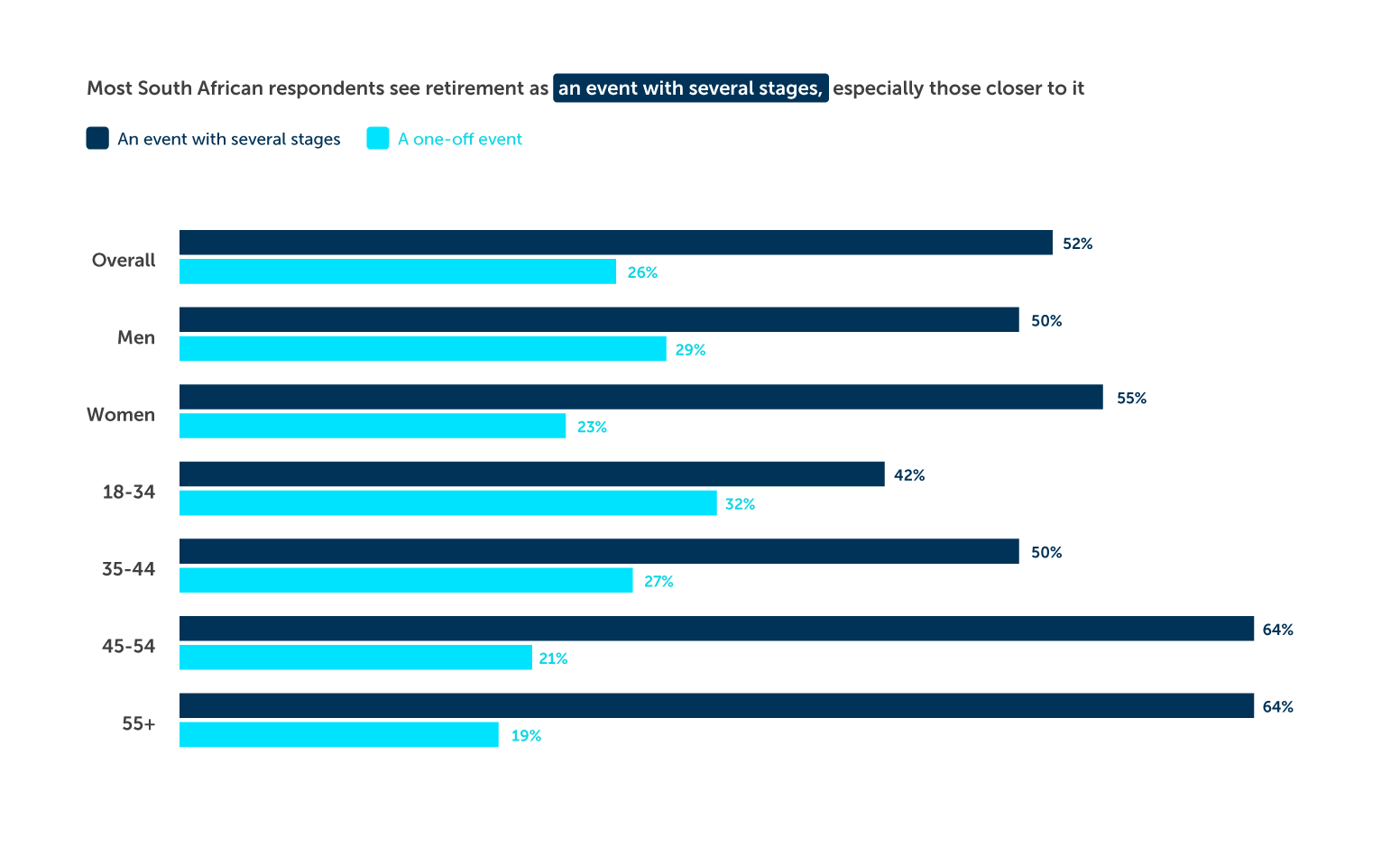

Around half (52%) of respondents in South Africa see retirement as an event with several stages, and just 26% see it as a one-off event. Many South Africans may work for longer and perhaps even never retire.

As is found in other regions, the view of retirement as a one-off event is more common among younger people (18-34), 32% of whom see retirement as a one-off change.

Healthcare and living costs drive retirement finance fears

Meeting basic costs is a worry when thinking about retirement

A significant number of South African respondents (61%) predict that their monthly costs will increase in retirement. This expectation is more common among younger people (63% of 18-34 year olds) than older people (56% of those aged 55+).

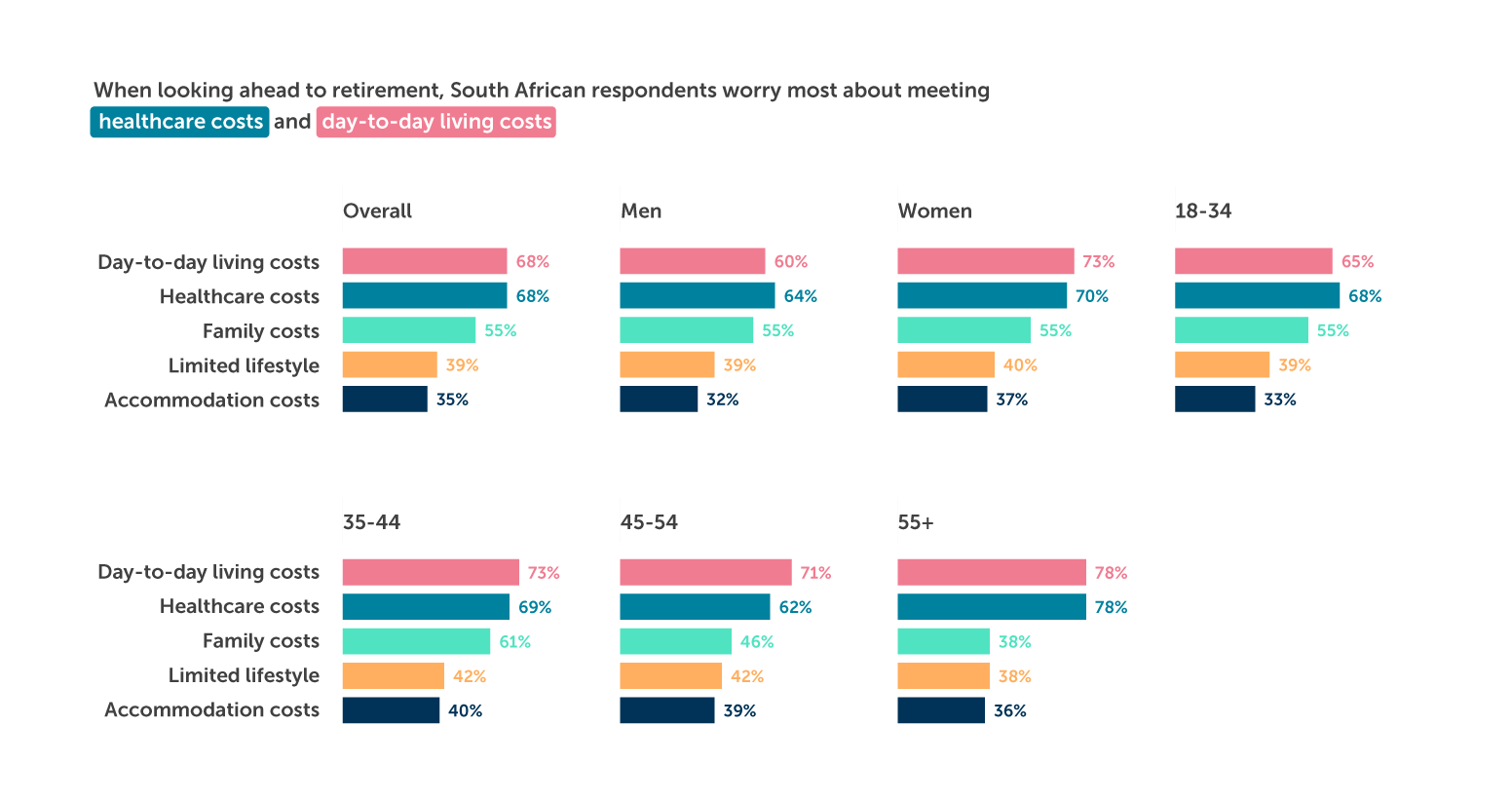

The biggest financial concerns for South African respondents during retirement are being able to afford both healthcare costs (68%) and day-to-day living costs (68%), with the costs associated with supporting family members a significant worry, too (55%). Women are particularly concerned about being able to afford day-to-day living costs compared to men (73% of women are concerned, compared to 60% of men), and also have heightened concerns about healthcare costs (70% of women are concerned compared to 64% of men).

When it comes to costs associated with supporting family members, younger people are more concerned than their older counterparts (55% of 18-34 year olds are concerned, compared to 38% of those aged 55+).

South African respondents are heavily dependent on personal savings to fund their retirement. Just 21% expect to rely on the government funded Older Person’s Grant and 49% on a private pension, while 61% will rely on personal savings. Younger people aged 18-34 are more inclined to say they will use their personal savings (63% compared to 44% of those aged 55+), and are less likely to say they will rely on an Older Person’s Grant (19% compared to 32% of those aged 55+).

People want flexibility and control

Respondents in South Africa are looking for autonomy in managing their retirement finances

Flexibility is crucial. When looking for a pension provider, the most important feature is a wide range of investment options – nearly two thirds of respondents (62%) say this is important.

Respondents in South Africa also want to have control. Their other top priorities are the ability to change their income amount if needed and to do so at the touch of a button. Almost all respondents (97%) consider it important that they can manage their retirement funds online.

A blended approach to financial management is the most preferred option in South Africa, with two thirds (65%) saying they want to manage their retirement finances themselves but with assistance. A small minority – just 6% – would like their finances to be managed entirely by someone else.

Clear, simple communication from pension providers is particularly important for older respondents, with almost three quarters (72%) of respondents aged 55+ listing it as important.

7 Retirement perceptions in Australia

When it comes to retirement saving, Australia’s highly-regarded superannuation system makes it the most advanced country of those covered in this report. It is mandatory for the vast majority of working Australians to save for retirement, particularly now the $450 per month threshold has been abolished. This has created high coverage and particularly benefited women, who are disproportionately likely to earn below the $450 threshold that previously meant employers were not obligated to contribute to retirement funds.

The system offers retirees considerable flexibility on spending or investing their savings, but this comes at a cost. Superannuation providers are now acknowledging that this freedom does not always result in the best outcomes. With this in mind, the Retirement Income Covenant has now come into effect, handing superannuation funds a responsibility to innovate so that their members can have improved financial outcomes in retirement.

The knowledge gap is shrinking

People’s understanding of retirement finance is improving

In 2021, just 56% of Australian respondents said they have a good understanding of the options available to them in retirement. This year, that figure has jumped to 69%.

Men (76%) are more likely to report having a good understanding than women (61%). Surprisingly, and in contrast to other countries surveyed, there is no significant difference between younger and older respondents.

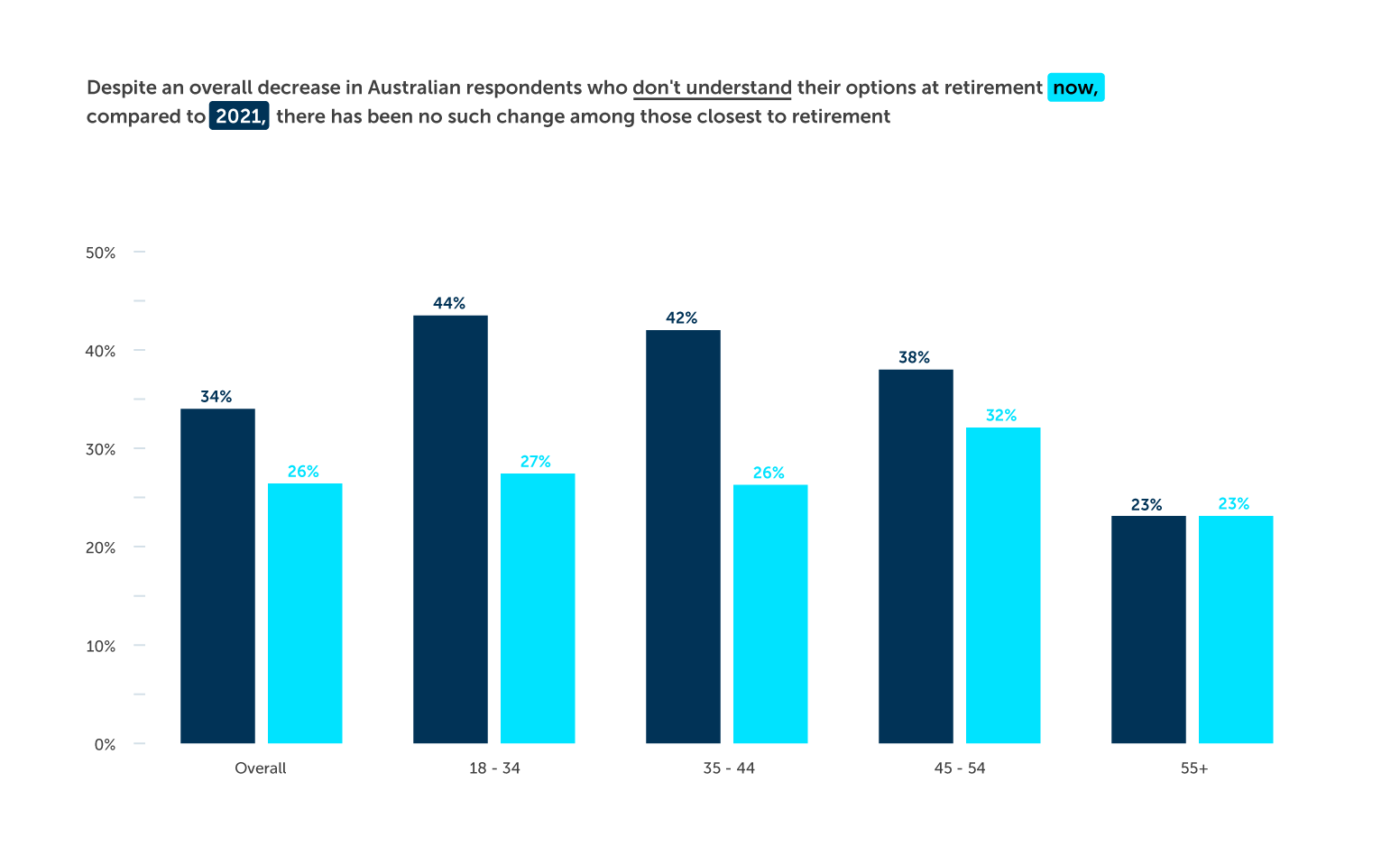

Although understanding of retirement finances is on the increase, almost a quarter (23%) of those aged 55 or older say they don’t understand their options. Given the high numbers of savers reaching retirement age in the next few years, this is a cause for concern. There remains a need to educate the population on where and how people’s money is being saved and what options are available on retirement.

Retirement is becoming a less fluid concept

Most still see retirement as a gradual process

Just under half of Australians (46%) see retirement as an event with several stages, a decrease from 55% in 2021. As is the case with other countries, younger people (aged 18-34) are more likely to see retirement as a one-off event (38%) than those aged 55+ (20%).

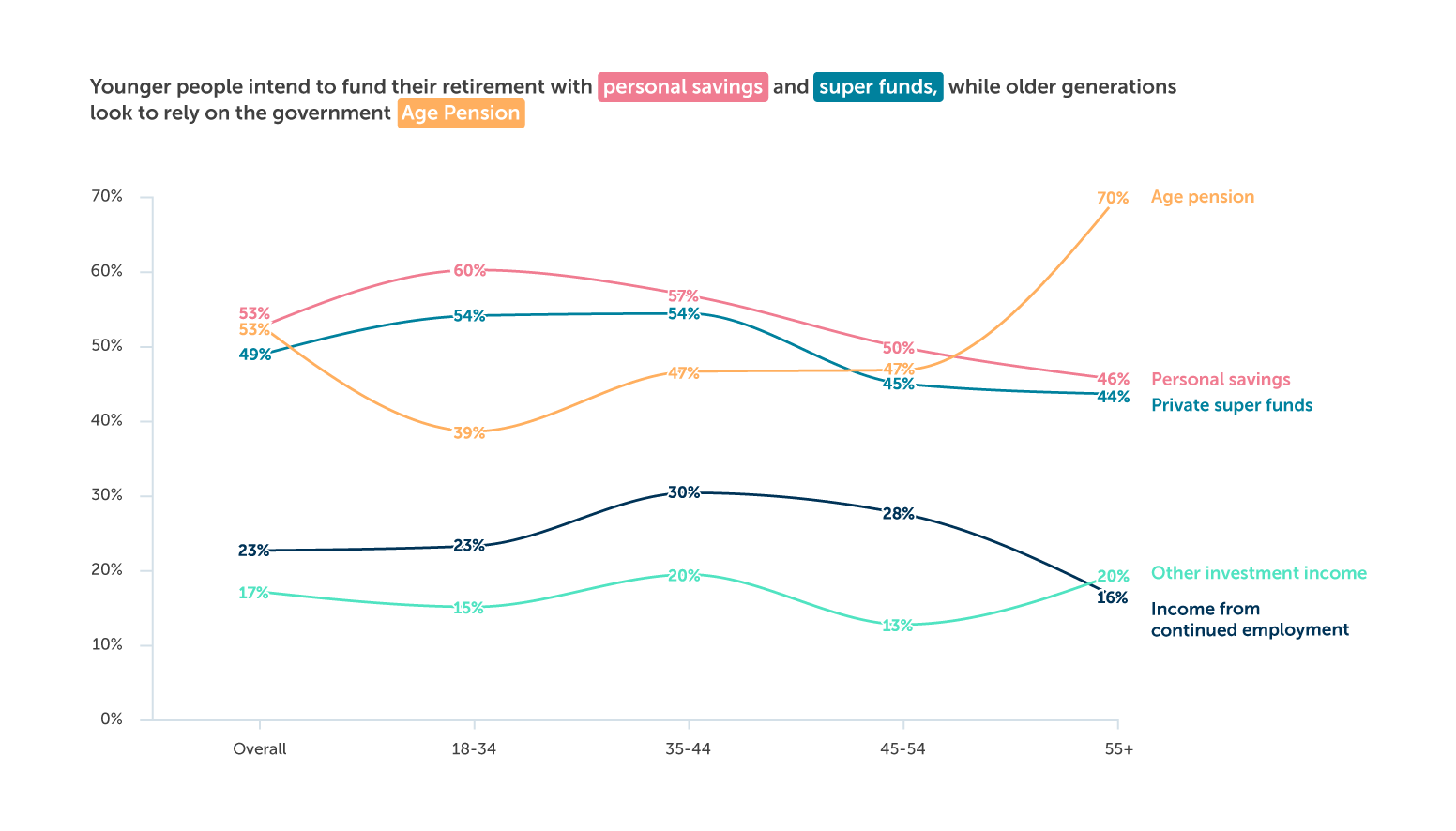

When it comes to financing their retirement, Australians appear just as likely to use their personal savings as they are to rely on their government funded Age Pension (53%). A super fund (retirement fund) is also an expected source of retirement income for 51% of Australians. Younger people (aged 18-34) are more likely to mention super funds (54%) than those aged 45+ (45%), probably due to the introduction of auto enrolment in the early 1990s.

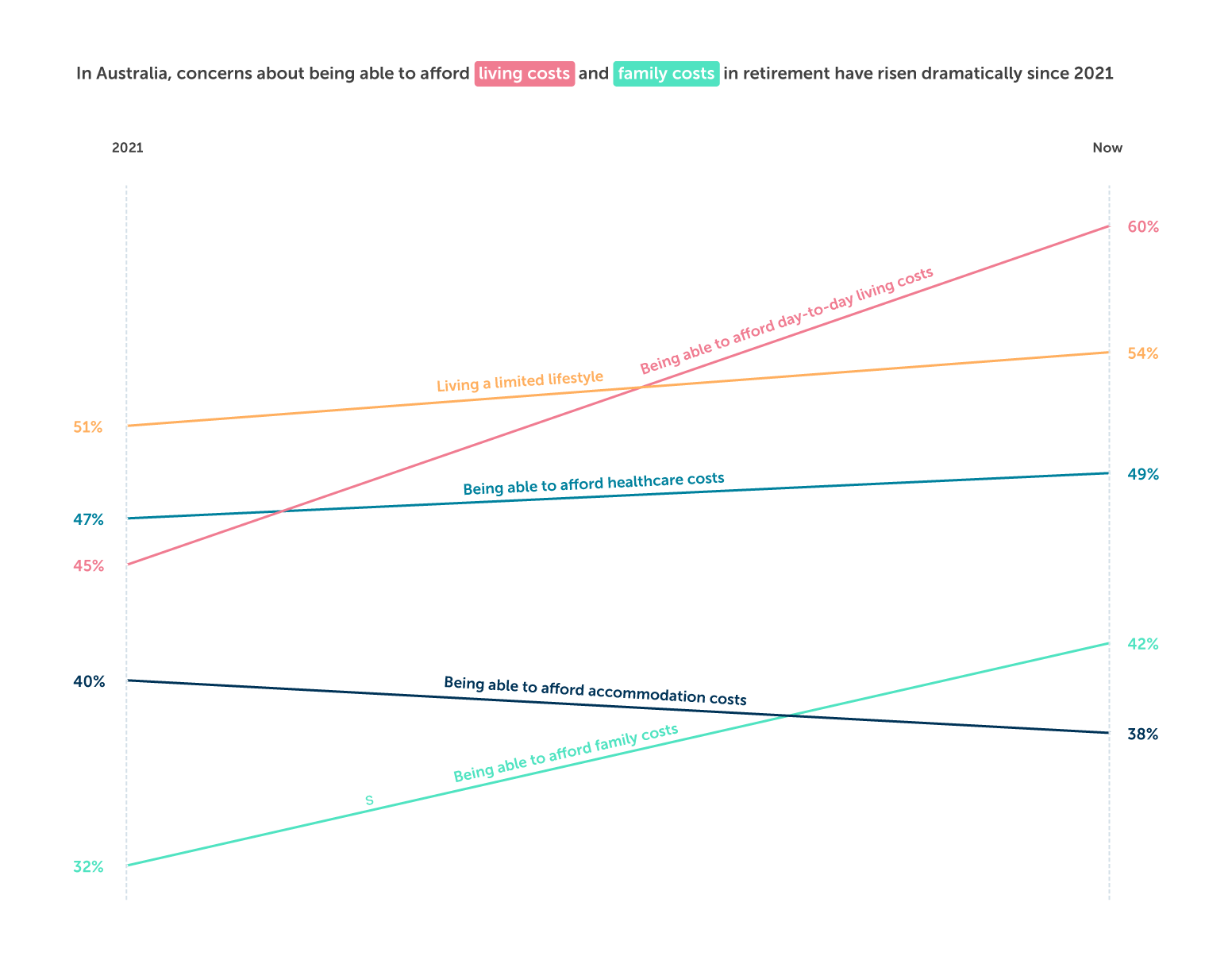

Retirement finance concerns go beyond the basics

Lifestyle options are a cause for worry alongside everyday costs

Being able to afford day-to-day living costs tops the list of Australian respondents’ financial worries when looking ahead to retirement (60%, up from 45% in 2021). This concern is strongest among women (65%, compared to 54% for men) and those nearing retirement, aged 55+ (63%, compared to 52% for those aged 18-34).

Australian respondents are also concerned about living a limited lifestyle in retirement, with 54% worried – a small increase from 51% in 2021.

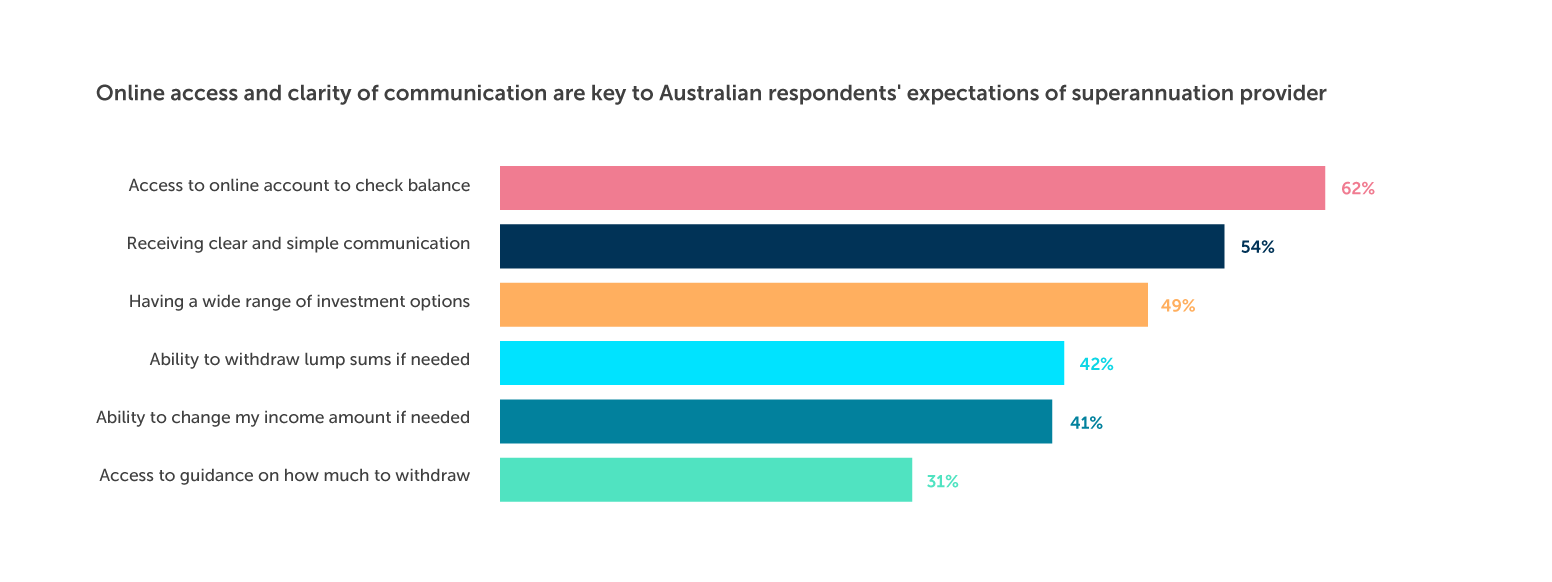

People want clarity and control

Clear information and a sense of autonomy are important

Australian respondents have an engaged, independent approach to seeking a retirement finance provider. Most important to them is the ability to check their balance online (62%), and their second priority is receiving clear and simple communications (54%).

Flexibility is increasingly important to Australian respondents. Around half (49%) say that having a wide range of investment options is important, a significant increase compared to 37% in 2021.

Among older Australian respondents, the ability to withdraw lump sums if needed is something of a prerequisite: 52% of those aged 55+ select this as important compared to 29% of those aged 18-34.

Nearly a third (30%) of Australian respondents want to manage their retirement finances entirely by themselves. This is driven by those closer to retirement – 43% of those aged 55+ would prefer to manage their finances alone, compared to 23% of those aged 18-34. About half (49%) of Australian respondents would prefer to manage their retirement finances with some assistance.

8 Summary

1) Understanding of pension options remains low

While people’s understanding of their retirement finance options varies across age and region, it remains lower than is ideal. This is particularly true of those approaching retirement age, whose understanding is better than that of younger generations but still worryingly limited. The varied economic context and legislation across regions means understanding varies geographically, and is lowest in Australia and the UK.

2) Concerns about living costs are shared across regions

Being able to afford day-to-day living costs is a key concern among all the regions surveyed. This is likely to reflect the current economic crisis, including inflation and rising living costs. It also reflects the fact that some retirement finance options are insufficient to reassure an ageing global population that they will have enough saved to continue their current levels of spending and quality of lifestyle into old age.

3) The gender gap persists

Reflecting continued gender inequality around the world, we found that women tend to be more concerned about living costs and healthcare costs than men across all the regions surveyed. The results also show that women’s understanding of their retirement finance options is slightly lower than men’s, and that women are more likely than their male counterparts to view retirement as a transition as opposed to a one-off event.

These differences reflect the significant gender pension gap that exists globally, and leaves women worse off in retirement. Auto enrolment into retirement savings schemes goes some way towards safeguarding savings for later in life, but there is more to be done to level the pension landscape in regards to gender and other demographics. Australia is leading the way here, with the most advanced defined contribution (DC) system of all those surveyed. Their example could guide other regions as they look to move to an auto enrolment setup.

4) Many savers’ needs aren’t being met

As we saw in 2021, there is a gap between what savers want from a pension provider, and what is being provided. This is particularly true of digital access, with many expressing an appetite for managing their retirement finances online, when the reality is that most will still receive paper statements. While other areas of life – like banking and shopping – are dealt with at the touch of a button, pension services lag behind. We can expect to see savers demand more of their pension providers in this space in the years to come.

As well as online access, all regions surveyed expressed an increasing desire for transparency and flexibility from their pension provider. Having a wide range of investment options is most important to Australians out of all the regions, perhaps representing their more advanced system.

We hope that highlighting the emerging needs, concerns and trends around retirement finance will help to shape the retirement landscape for the better. This is just one example of the types of research we do to inform our development of technology solutions that make pensions simpler and more accessible for all.

9 Keystone by Smart

Keystone by Smart is the first global, cloud-native, workplace retirement savings platform.

We designed it for governments, large organisations and financial institutions who need a customisable Platform as a Service (PaaS) solution. It is now live on four continents, in partnership with some of the best-known financial institutions in the world, helping over a million savers plan for, and manage their money in, retirement.

Over a million hours of R&D have gone into developing Keystone. It enables everything from apps and web-based tools for employers and employees to full data migrations. Our partners can move or consolidate hundreds of thousands of accounts with ease, and feel confident that the platform can be adapted to incorporate changes in legislation now or in the future. www.smart.co/what-we-do/keystone

10 Archive

Downloads:

The Future of Global Retirement 2021

The Future of Global Retirement: The Netherlands

11 Appendices

11.1. Detailed methodologies

United States and Australia survey methodology

https://visit.smart.co/pollfish

US data weighting

Survey results for the US were weighted by age, gender and income using data extracted from the American Community Survey’s five-year data, collected from ~120,000 households. This is widely considered a reliable source of US demographic data. The data was weighted using iterative proportional fitting, a standard weighting procedure.

Australia data weighting

Survey results for Australia were weighted by gender and age group from the publicly available 2021 census data. The data was weighted using iterative proportional fitting, a standard weighting procedure.

United Kingdom survey methodology

11.2. Further information

For further information on this report, on Smart, or on our Keystone technology platform, contact pressoffice@smart.co, or visit www.smart.co.